Muzinich Weekly Market Comment: It could have been worse

Insight

August 3, 2026

If you have any feedback on this article or are interested in subscribing to our content, please contact us at opinions@muzinich.com or fill out the form on the right hand side of this page.

--------

July defied its reputation as one of the year's most dependable months. As geopolitical tensions, AI-related capital expenditure and a more ambiguous Federal Reserve converged, investors increasingly found themselves pricing uncertainty rather than simply fundamentals.

July is normally one of the strongest and most dependable months of the year, the kind of month investors expect to coast through. This one was anything but. Rather than the usual seasonal tailwind, the month forced investors to grapple with the extraordinary on three fronts at once. Geopolitically, there was the stop-start conflict in the Middle East and the surrounding aggressive rhetoric. On valuations, investors wrestled with the viability of AI business models, the associated demand for semiconductors and raw compute, and the ever-growing, front-loaded capital investment those ambitions require. Economically, markets had to re-price two shifts in policy backdrop: a new Federal Open Market Committee (FOMC) reaction function under Chair Warsh and a new prime minister in the UK.

In fixed income, government bonds underperformed. European curves bore the brunt of the Middle East geopolitics, shifting higher in a broadly parallel fashion, while the US fared slightly better, particularly at the front end, with the curve bear-steepening as investors reset the Federal Reserve (Fed) reaction function. Japanese government bonds outperformed, the curve bear-flattening as the Bank of Japan (BOJ) hinted it may accelerate its policy cycle.

In credit, high yield beat investment grade, generating positive excess returns over governments in both emerging markets (EM) and European high yield, though on a total-return basis the only genuine haven was short-duration high yield.

In currencies, the US dollar appreciated against the major global currencies, and in commodities, energy finished the month up over 20%. European equities had a solid month, with the FTSE (Financial Times Stock Exchange) up over 3% and the Euro Stoxx 50 close to 1%. Meanwhile US equities lagged their developed-market peers, dragged down by the technology sector; even so, that drag was modest compared to South Korea's KOSPI (Korean Composite Stock Price Index), down more than 20% on the month.

In Asia, China's Politburo convened its mid-year meeting, with economic policy high on the agenda. The readout was stronger on rhetoric than on specifics, but the main takeaway was that the committee gave the green light for further monetary and fiscal loosening in the second half.1 In Japan, the BOJ held its target rate at 1%, in line with expectations. Governor Kazuo Ueda flagged three risks the Bank is watching closely – the Middle East, AI-related demand, and the yen – noting that it will take time for the impact of the June rate hike to filter through the economy.2 That last point nudged investor expectations for the next move back to December, when the policy rate is anticipated to rise to 1.25%.

In Europe, it was a heavy week for economic data. Euro-area HICP (Harmonised Index of Consumer Prices) inflation ticked up a touch in July to 2.9% year-over-year (YoY) from 2.8% in June. Given the 20% rise in energy prices, it was little surprise that energy contributed most to the increase. Core inflation, however, surprised to the upside, rising to 2.5% against expectations that it would hold unchanged at 2.4%.3 That came alongside the good news of stronger-than-expected second-quarter GDP in the Eurozone, where output rose a solid 0.4% quarter-over-quarter, above the 0.2% consensus. The strength was broad-based, with all four of the bloc's largest economies surprising to the upside.4 Taken together, hotter core inflation and firmer growth could give the ECB (European Central Bank) the green light for a September hike, with the overnight index swap market implying a 90% likelihood.

In the UK, the Bank of England held rates steady at 3.75%, with officials continuing to balance the threat from the US-Iran conflict against limited signs of domestic price pressures. "There is little evidence yet of second-round effects, although it is too early to take much comfort from that," said Governor Andrew Bailey.6 He framed the decision as one of competing forces: "Holding bank rate is appropriate as global conditions look to be more uncertain and inflationary, while domestic conditions are, on balance, more benign." The overnight index swap market does not price in a full 25bp hike until December.5

As for the US, the FOMC meeting ought to have been a low-key event. The committee voted in line with expectations, 9–3, to hold the federal funds target range at 3.50%–3.75% for a seventh straight month. The accompanying statement also offered investors very little to analyze. At just 197 words, it differed from June's statement by the removal of only seven words.7 Then everything changed during Chair Warsh's press conference. He delivered an unequivocally hawkish message on inflation: "There is no soft inflation target…. Not on this committee's watch. There's only a target, and it's 2%."8 Those remarks triggered an avalanche of questions centered on one apparent contradiction: if the Fed is so hawkish, why didn't it raise rates?

Warsh's answer was that financial conditions had already tightened without the need for further policy action. Nominal Treasury yields had risen meaningfully between the June and July meetings, and, in his view, reflected investors responding to stronger-than-expected economic data rather than anticipating a higher policy rate. As he put it, "Market participants are learning to play the ball, not the referee".8

He also refused to pre-position expectations for Jackson Hole, describing it as "a blank page".9 That comment added another layer of uncertainty, leaving markets questioning how serious the Fed is about preparing the ground for a future rate increase.

Henry Kissinger, who made the approach famous through his diplomatic style in the 1970s, particularly during Middle East negotiations, is often credited with the concept of constructive ambiguity: the deliberate use of imprecise language that allows parties who do not fully agree to endorse the same outcome, each interpreting it in their own way. The ambiguity is "constructive" because it serves a useful purpose.

Applied to central banking, constructive ambiguity means deliberately avoiding guidance about future policy. By keeping its intentions opaque, the central bank preserves flexibility, avoids being boxed in by previous statements, and prevents markets from simply front-running a pre-announced policy path. Instead, investors are forced to continually reassess incoming data and form their own expectations.

Fed Chair Warsh has taken this a step further, into what is better described as explicit constructive ambiguity. Ordinarily the ambiguity is implicit: the central banker is vague and lets investors infer that the vagueness is deliberate, never quite admitting the game. What's notable about Warsh is that he isn't hiding it. He openly states that he has withdrawn forward guidance and pared statements back to the minimum. The "blank page" remark on Jackson Hole is the clearest tell: the opacity is not an accident of communication; it is the design.

If we decompose a government nominal yield, it consists of three broad components: an expected real rate (the growth piece), the expected inflation over the life of the bond, and a residual – the term premium. The term premium is the compensation investors demand for uncertainty about the path of policy. That is, the fee for holding a long, path-dependent asset when the path is unknown. The more uncertain the path, the bigger the fee.

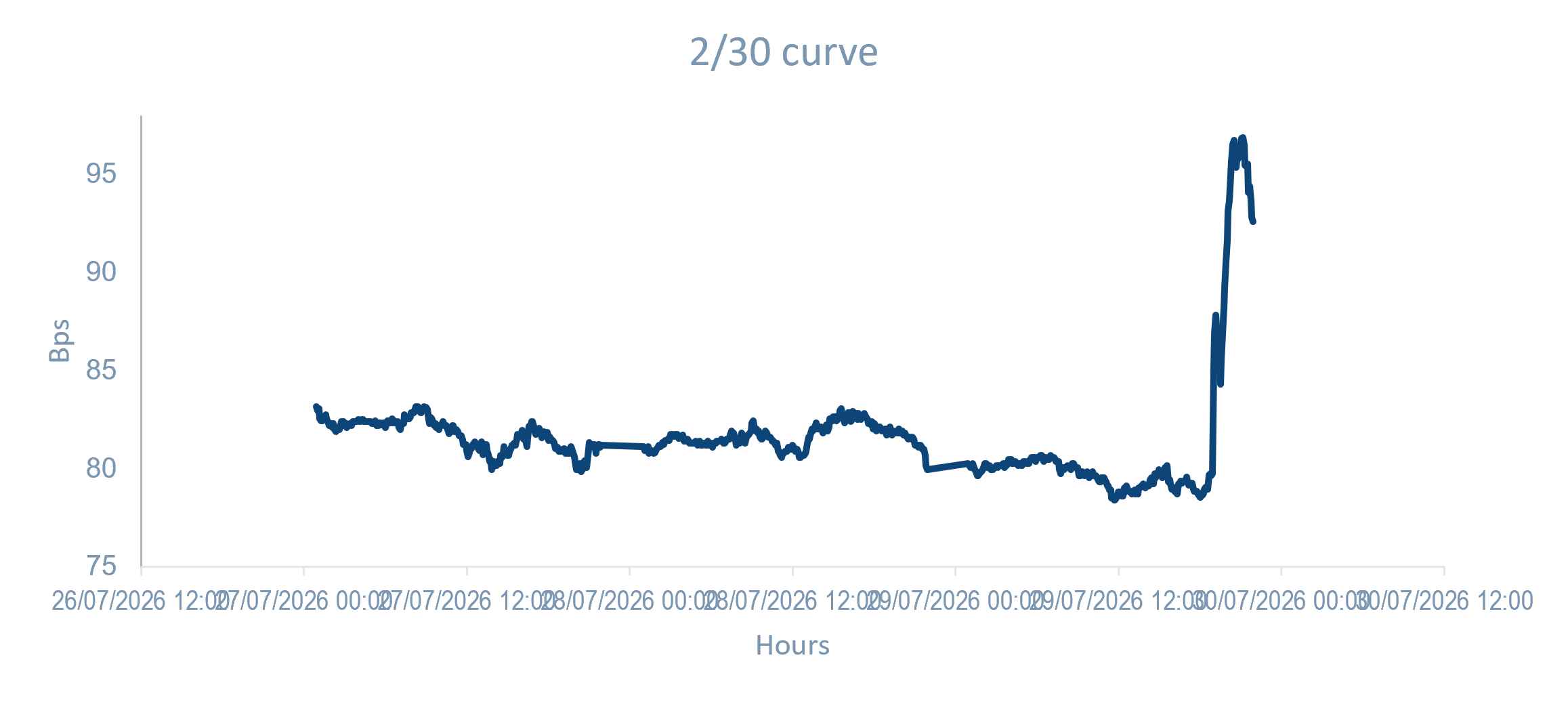

Heavy forward guidance is how a central bank depresses that fee. By telling investors the likely path of rates – or at least the reaction function it will follow –the central bank absorbs a chunk of investor uncertainty. The central bank does the forecasting and commits, at least reputationally, to that forecast. With less uncertainty about where rates are headed, investors demand less compensation, and the term premium shrinks. In effect, the central bank is selling investors insurance policies against the unpredictability of the economy. By withdrawing that guidance, the Fed is effectively cancelling the insurance policy. That is, uncertainty lands back on the investors' shoulders, so the term premium must rise; investors will demand compensation for the uncertainty against which they are no longer insured. This largely explains the steepening of the US curve after the policy meeting, with the 2/30 rising 15bps. See Chart of the Week.

Mathematically, this is a second-moment effect, an increase in variance. That is, a widening in the distribution of outcomes regardless of direction as the range of plausible paths has fanned out. Or put simply, investors should expect greater volatility from government yields under Chair Warsh.

The other two components of the yield – growth and inflation expectations – behave differently. These are first-moment effects, equivalent to the mean of the distribution, and unlike the term premium, they are directional: they can move up or down. The crucial point is that Warsh only took away the Fed's own commentary. He didn't change the actual growth and inflation numbers.

That leaves two questions. First, had the prior Fed's guidance been pulling expectations away from where the data alone would put them? This may help explain the bearish move in US rates last week, which is not what the data alone would suggest, as both the key growth and price reports came in soft: real GDP growth cooled to 1.5% in the second quarter from 2.1% in the first,10 and the PCE (Personal Consumption Expenditures) deflator actually fell 0.11% in June (against +0.46% prior), pulling the YoY rate down to 3.7% from 4.1%, with core PCE slowing to 0.13% in June. At an annualized rate, core PCE inflation cooled to 1.6% on a one-month basis (vs. 4.1% prior) and 2.9% on a three-month basis (vs. 3.6% prior). On that data, yields would normally have fallen.

Second, in which direction would the Fed adjust going forward? Here Warsh's reputation is decisive. Ambiguity from a known inflation hawk is not an invitation to price more inflation; it’s a warning that any hot pricing data could be met with a forceful response. That works to anchor inflation expectations but raises the directional volatility of the yield in response. In other words, we should expect yields to react more sharply to strong inflation data than weak prints going forward, even as inflation expectations themselves stay contained.

On that reading, bond investors may have been fortunate that the PCE report came in soft. And perhaps that is the best way to sum up July in a single sentence: “It could have been worse.”

Chart of the Week: Term Premium; Investors demand higher compensation for uncertainty in the Warsh era

Source: Bloomberg, as of July 31, 2026. Muzinich views and opinions are subject to change. For illustrative purposes only, not to be construed as investment advice or an invitation to engage in any investment activity.

Past performance is not a reliable indicator of current or future results.

References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of July 31st, 2026, and may change without notice. All data figures are from Bloomberg, as of July 31st, 2026, unless otherwise stated.

References

1. Citi Research China Economics, “Mid-Year Politburo: Rate Cut Green Light, Fiscal Acceleration Ahead,” July 30, 2026

2. Bloomberg, “BOJ REACT: Ueda’s Mixed Signals Tilt Toward Wait-and-See,” July 31, 2026

3. Bloomberg, “EURO-AREA REACT: Higher Core, Strong GDP Lift ECB Hike Case,” July 31, 2026

4. Bloomberg, “EURO-AREA REACT: Strong GDP Bolsters ECB September Hike View,” July 30, 2026

5. Bloomberg, as of July 31, 2026

6. Bloomberg, “BOE Holds Rates in 6-3 Vote as War Clouds Inflation Outlook,” July 30, 2026

7. Bloomberg First Word, “The Market Is Forecasting the Fed Around a Corner: Macro Man,” July 29, 2026

8. MT Newswires, “Fed Chair Warsh Says 2% Inflation Target Remains, Markets Focused on Events, Not Fed,” July 29, 2026

9. Bloomberg, “Why Markets Are Already Having Trouble Translating Warsh-Speak,” July 30, 2026

10. Bloomberg, “US REACT: Domestic Demand Resilient Despite Inflation Pressures,” July 30, 2026

--------

Important information

Muzinich & Co., “Muzinich” and/or the “Firm” referenced herein is defined as Muzinich & Co. Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability, heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. Any forward-looking information or statements expressed in the above may prove to be incorrect. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Muzinich gives no undertaking that it shall update any of the information, data and opinions contained in the above.

United States: This material is for Institutional Investor use only – not for retail distribution. Muzinich & Co., Inc. is a registered investment adviser with the Securities and Exchange Commission (SEC). Muzinich & Co., Inc.’s being a Registered Investment Adviser with the SEC in no way shall imply a certain level of skill or training or any authorization or approval by the SEC.

United Arab Emirates (UAE): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the UAE. It is intended solely for Professional Investors and should not be relied upon by any other person. This material has not been reviewed or approved by the UAE Securities and Commodities Authority, the UAE Central Bank or any other relevant authority. Nothing contained herein constitutes investment, legal, tax or other professional advice. Recipients should make their own independent assessment where appropriate.

Abu Dhabi Global Market (ADGM): This information is provided for discussion and informational purposes only and does not constitute an offer or solicitation in the ADGM. It is intended solely for Professional Clients (as defined by the Financial Services Regulatory Authority) and should not be relied upon by any other person. This material has not been reviewed or approved by the Financial Services Regulatory Authority or any other relevant authority in the UAE.

Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Registered in Ireland, Company Registration No. 307511. Registered address: 32 Molesworth Street, Dublin 2, D02 Y512, Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland. Issued in Singapore and Hong Kong by Muzinich & Co. (Singapore) Pte. Limited, which is licensed and regulated by the Monetary Authority of Singapore. Registered in Singapore No. 201624477K. Registered address: 6 Battery Road, #26-05, Singapore, 049909. Issued in all other jurisdictions (excluding the U.S.) by Muzinich & Co. Limited. which is authorized and regulated by the Financial Conduct Authority. Registered in England and Wales No. 3852444. Registered address: 8 Hanover Street, London W1S 1YQ, United Kingdom.

By clicking "Submit", I am (i) signing up to receive the Opinion Pieces from the "Opinions" page of the Muzinich & Co website, (ii) representing that the above information is true and accurate and (iii) agreeing to join the Muzinich & Co mailing list. I understand that Muzinich & Co will not add retail investors or individuals with personal email addresses to its mailing list and represent that I am not a retail investor. By providing my personal and professional information I am consenting to its use and disclosure in accordance with the Muzinich & Co. Privacy Policy. I understand that I may withdraw my consent and unsubscribe from receiving future communications by clicking "Unsubscribe" from the emails that are sent to me from Muzinich & Co.